The European Commission published on March 18, 2026 its proposal for a groundbreaking “28th company law regime” called EU Inc., aimed at unifying fragmented national rules for limited liability companies across the EU. The EU Inc. framework provides an optional, harmonised company structure available across the EU to innovative startups and scale-ups companies. With two essential notes: the new regime does not replace national company law regimes, while taxation remains within the sole competence of Member States.

By Mihaela Gorun, Senior Tax Manager Taxhouse

Why EU Inc.?

The proposal comes as a response to the 2024 Draghi Report(1) which highlighted the EU’s urgent need to focus on improving its competitiveness. Per the Dealroom database(2), Europe had only 331 unicorns compared with 1963 in the U.S as of 2025.

Mario Draghi, former president of the European Central Bank, pointed out in that report – written in a less tense geopolitical context than the current one – that excessive regulation reduces Europe’s ability to develop companies capable of competing on an equal footing with those in America and China.

“Any entrepreneur will be able to create a company within 48 hours, from anywhere in the European Union and fully online.” , summarized Ursula von der Leyen, President of the European Commission, the essence of the new initiative.

What does “innovative” mean?

As there is currently no single EU definition of those companies, the Commission has adopted a Commission Recommendation(3) on the definitions of innovative enterprises, innovative startups and innovative scaleups:

- An “innovative enterprise” is one that either:

- Spent ≥10% of operating costs or ≥5% of net sales on R&D in at least one of the past three years, or

- Has recently developed or is developing new or significantly improved products, services, or processes that carry technological or industrial risk.

- Innovative startup: a small, autonomous innovative enterprise with fewer than 100 employees, turnover or assets under €10 million, and less than 10 years of operation.

- Innovative scaleup: is an autonomous, innovative enterprise with turnover or assets above €10 million, growing over 20% annually in employees or revenue for the past two years, and either employing fewer than 750 people or not being publicly listed.

Core Features of the EU Inc. Regime

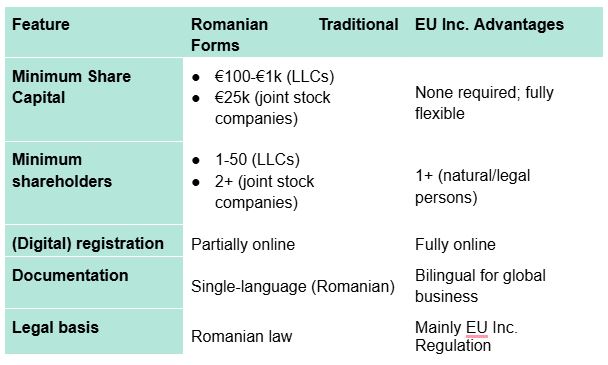

The EU Inc. framework is desiged to be implemented by way of a Regulation all across the EU – hence, it will have direct and automatic applicability in all Member States – offering a digital‑first corporate legal form as an alternative to the 27 national systems and their 60+ company types.

- Fast digital setup: EU Inc. companies can be registered online from any Member State within 48 hours, for under €100, with no minimum capital. They will use the “EU Inc.” suffix to signal standardised features and build trust.

- Simple procedures: A central EU register will store all company data, enabling automatic issuance of tax and VAT numbers without repeated submissions. Existing companies can convert, merge, or spin off subsidiaries smoothly, in line with local employee participation rules.

- Digital insolvency: Liquidation will be fully digital and generally completed within 3–6 months, subject to specific conditions.

- Cross-border operational efficiency: The proposed European Business Wallet will allow EU Inc. companies to handle all cross‑EU dealings – tax filings, permits, contracts – fully digitally and with legal validity, using stored company data and without any physical documents or in‑person steps.

What does EU Inc. mean tax-wise?

- Taxation remains the exclusive competence of Member States: Although the legal status of an EU Inc. company allows for the harmonisation and centralisation of certain tax reports, this legislative framework does not aim to establish a harmonized tax regime at EU level. Consequently, the fees and duties owed by both an EU Inc. company and its shareholders will be determined in accordance with the tax regulations applicable in each Member State. For example, an EU Inc. company registered in Romania will be subject to the same tax obligations as a classical LLC, including, but not limited to:

- corporate income tax, applied at the stadard flat rate of 16%;

- the obligation to withhold tax on dividends distributed to shareholders;

- the obligation to apply withholding tax on income paid to non-residents, in accordance with the Romanian Tax Code and the applicable double tax treaties.

At the same time, the shareholders of EU Inc. – regardless of whether the company is registered in Romania or in another Member State – will continue to owe capital gains tax in Romania, as long as they qualify as Romanian tax residents.

- EU common scheme for employee stock options (EU-ESOs): EU Inc. companies may opt into the EU-wide ESO under which options are taxed only when the shares are sold. Taxable income is calculated uniformly as the difference between the fair market disposal value and acquisition price, while Member States remain free to set the tax rates and classification – though the Commission encourages treating gains as capital gains. Eligibility is limited to board members and employees who do not hold (and have not held in the past 24 months) more than 25% of voting or profit rights. The scheme also requires a minimum 24‑month vesting period (the period after which employees may acquire the shares).

- Harmonising social security for EU‑wide remote work: The Commission will assess allowing startups and scaleups to telework 100% cross‑border while remaining under the social security system of the employer’s Member State. To support this, a legal framework will be developed to digitalise social security attestations through the European Social Security Pass initiative.

- Once-only submission of information: Company information, including details on its branches, will be shared automatically from the business register with relevant tax, social security, and anti‑money‑laundering authorities, so the company does not need to resubmit it. TIN and VAT numbers will be issued at registration, except in limited cases where additional information is required by the local VAT authority.

- Streamlined shares transfers: Share transfers for EU Inc. companies can be completed fully digitally, without requiring any intermediaries; this may also make the capital gains administrative procedures less burdensome.

- Tax clearance certificates for fast-track liquidation: The tax authority has 30 days—extendable once by up to 30 days—to issue clearance or object to a fast‑track liquidation. If it does not respond within the deadline, clearance is assumed.

- Preventive control: EU Inc. companies will face the same preventive controls as traditional companies to prevent abusive or fraudulent letter-box structures tied to tax evasion or money laundering.

- Safeguarding measures: A blacklist of prohibited national practices will ensure EU Inc. companies receive equal treatment to national LLCs. For example, they cannot be required to establish a local presence to access state aid, operate, obtain authorisations, or use a bank account from another Member State.

EU Inc. vs. the U.S. Delaware regime – similarities and differences:

- General tax framework: Delaware offers strong state‑level tax advantages – such as no corporate income tax on non‑Delaware‑sourced income – making it attractive for for holding companies or remote operations, though the 21% U.S. federal tax still applies on worldwide income. EU Inc., by contrast, leaves taxation entirely to national rules (EU average CIT in 2026 is 21.6%) and provides no EU‑wide tax exemptions for cross‑border activity.

- Startup-Specific Tax Perks: Delaware allows unlimited loss carryforwards and may grant up to a 100% capital-gains exclusion for Qualified Small Business Stock. EU Inc. provides only one harmonised benefit: taxation of EU-ESO stock options is deferred until share disposal.

- Non-Resident and Cross-Border Treatment: Non-U.S. owners of Delaware companies are generally exempt from U.S. tax on income earned abroad, though some withholding may apply. EU Inc. subjects non-EU investors to domestic withholding taxes (e.g., on dividends) and potential CFC (Controlled Foreign Company) rules.

Potential draw-backs / areas for improvement

EU Inc. companies must still choose a national jurisdiction and comply with local rules – such as employee participation, labour law, and taxation – so entrepreneurs may still face 27 different regulatory environments despite harmonised corporate rules.

Although the Commission proposes specialised national courts for EU Inc. disputes, if these are not created, cases will remain in national courts without a unified EU‑level judicial mechanism.

Conclusion & Next steps

Overall, the EU INC. regime may prove quite attractive for EU operations – especially where EU market focus justifies local compliance burden – despite the fact that currently no tax harmonization is contemplated for this regime.

In other words, the main advantage of the EU Inc. regime is the digitization and debureaucratization of a significant number of corporate operations, which, in Romania, can considerably reduce the administrative burden and generate significant savings in time and resources (including financial).

The EU Inc. proposal will now proceed to negotiations in the European Parliament and the Council, with the Commission aiming to support both institutions to secure an agreement by the end of 2026.

1 Mario Draghi, “The Future of European Competitiveness – A Competitiveness Strategy for Europe” (report, European Commission, September 2024).

2 Consulted on 16 March 2026

3 Commission Recommendation (EU) 2026/720 of 18 March 2026 on the definition of innovative enterprises, innovative startups and innovative scaleups